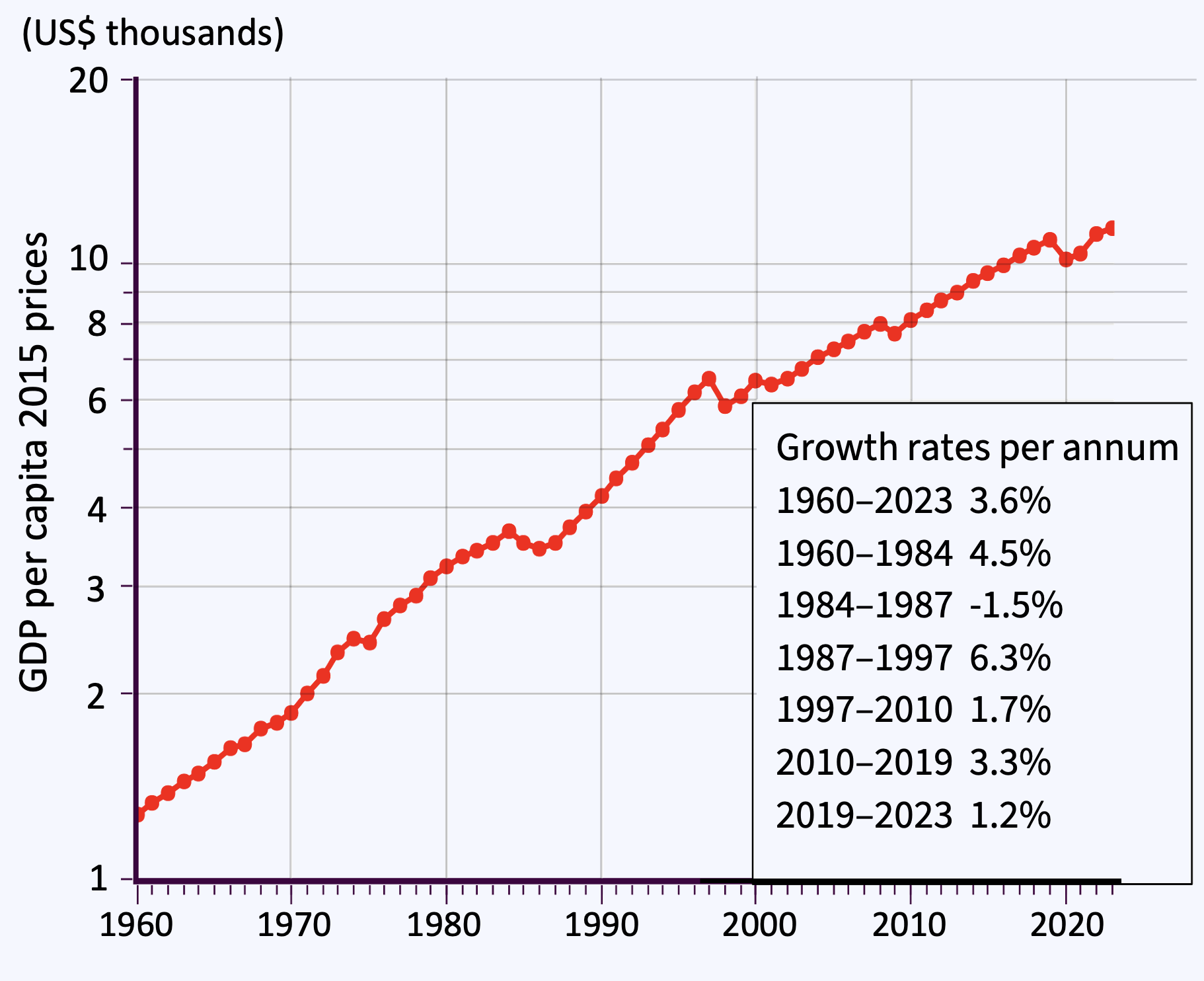

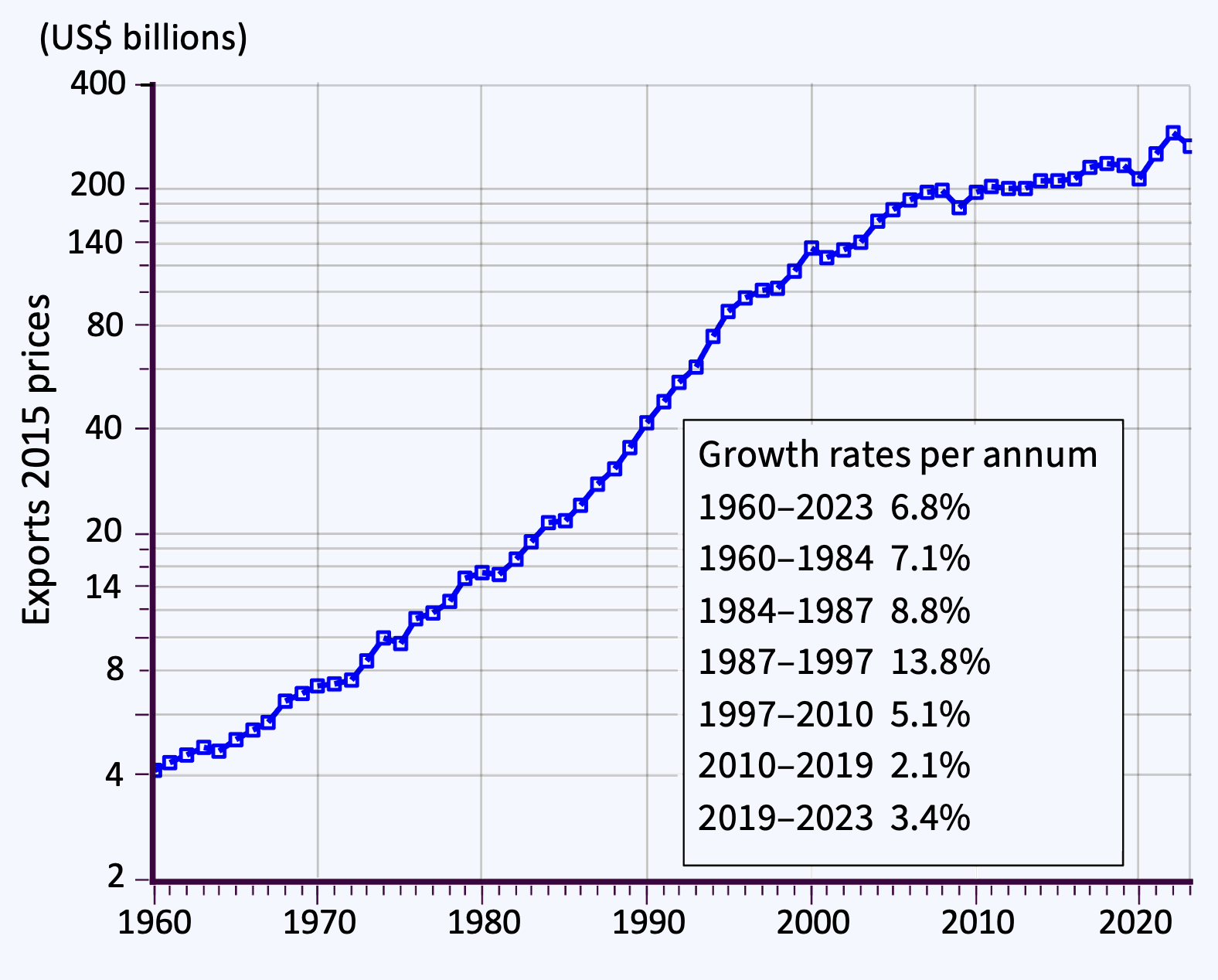

Export-led growth

Global value chains

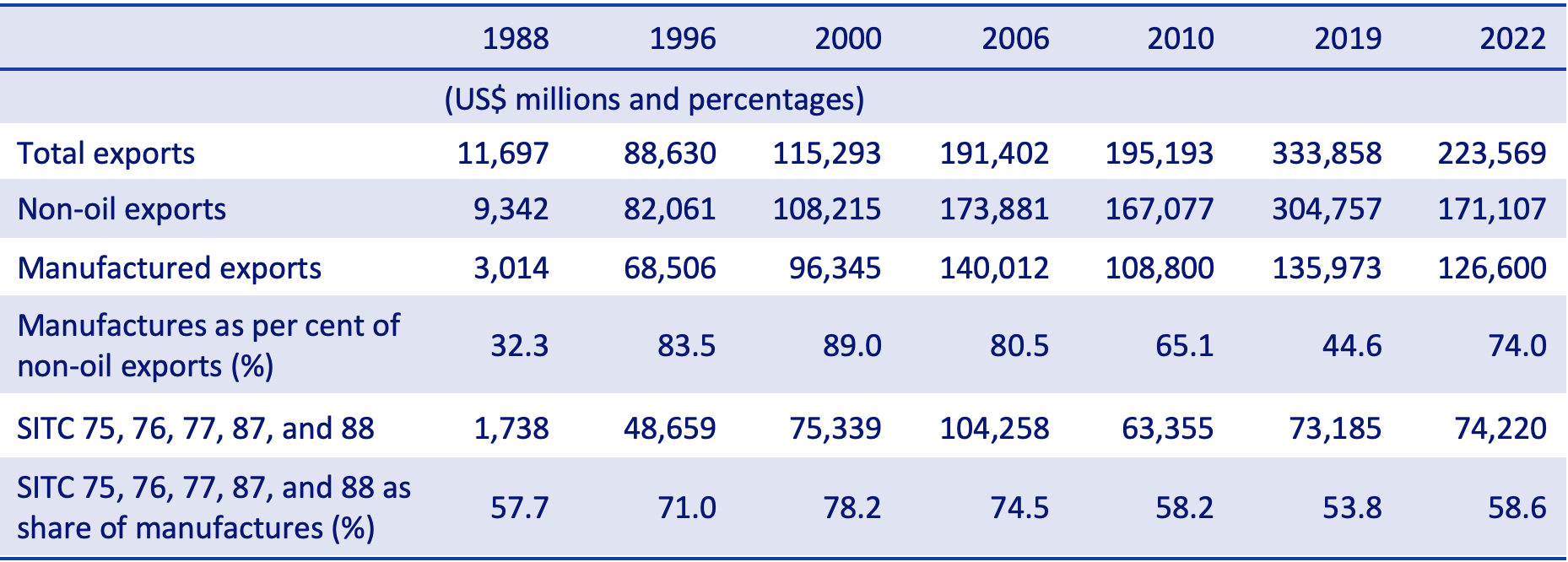

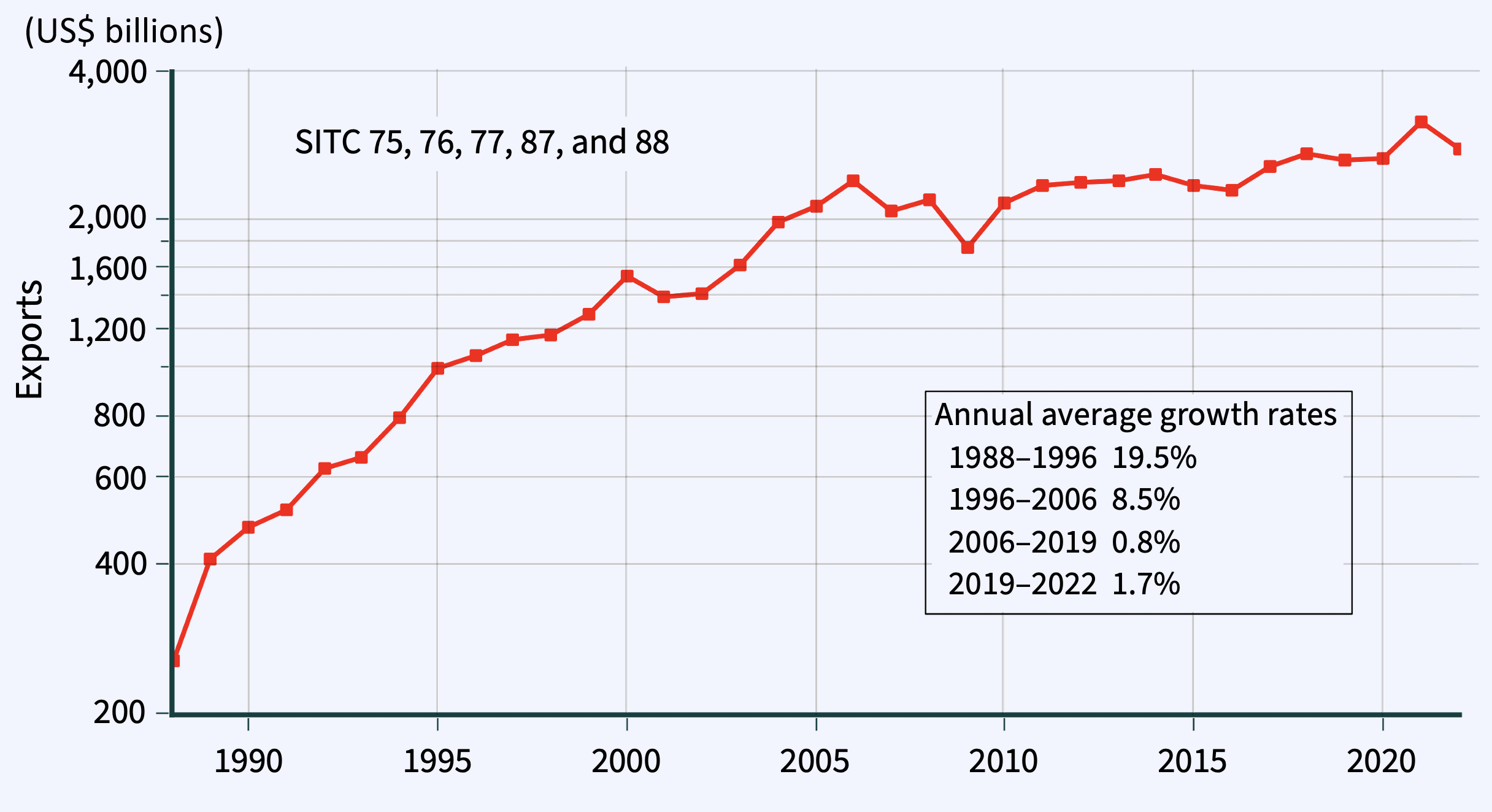

Global electronics industry

Malaysian electronics industry

Migrant labour

Education and development

Way forward

Baldwin, R. E. 1956. ‘Patterns of Development in Newly Settled Regions’. The Manchester School, 24/2, pp. 161–179.

______ 1963. ‘Export Technology and Development from a Subsistence Level’. The Economic Journal, 73/289, pp. 80–92.

Caves, R. E. 1965. ‘“Vent for Surplus” Models of Trade and Growth’, in Baldwin, R. E. et al. (eds), Trade, Growth and the Balance of Payments. Chicago: Rand McNally, pp. 95–115.

______ 1971. ‘Export-led Growth and the New Economic History’, in Bhagwati, J. N. et al. (eds), Trade, Balance of Payments and Growth. Amsterdam: North Holland, pp. 403–442.

Economic Planning Unit–Malaysia (EPU–M). 1971. Second Malaysia Plan, 1971–1975. Kuala Lumpur: Government Printers.

Edgington, D. and Hayter, R. 2013. ‘The In Situ Upgrading of Japanese Electronics Firms in Malaysian Industrial Clusters’. Economic Geography, 89/3, pp. 227–259.

Frederick, S. and Gereffi, G. 2016. The Philippines in the Electronics & Electrical Global Value Chain. Durham. NC: Center on Globalization, Governance & Competitiveness, Duke University. https://dukespace.lib.duke.edu/items/88a06165-8a8e-462b-a2c1-1a3d29f7fb49

Hawati Abdul Hamid. 2022. Malaysian Higher Education and Economic Growth: A Causality Analysis. Working paper 3/22, 28 October. Kuala Lumpur: Khazanah Research Institute.

Hirschman, A. O. 1989. ‘Linkages’, in Eatwell, J., Milgate, M. and Newman, P. (eds), The New Palgrave: Economic Development. London: Macmillan, pp. 210–221.

Hutchinson, F. E. 2008. ‘“Developmental” States and Economic Growth at the Sub-national Level: The Case of Penang’. Southeast Asian Affairs, pp. 223–244.

Intarakumnerd, P. and Jutarosaga, A. 2023. ‘The Evolution of University–Industry Linkages in Thailand’. Asian Economic Policy Review, 18/2, pp. 265–282.

Koay S. L. 2024. Penang’s Industrialization and Economic Transformation, 1960s to 1980s. https://www.ehm.my/publications/articles/penangs-industrialization-and-economic-transformation-1960s-to-1980s.

Lee, C. 2023. ‘Comment on “Transforming Malaysia’s Higher Education: Policies and Progress”’.Asian Economic Policy Review, 18/2, pp. 261–2.

Malay Mail. 2024. ‘Malaysia Takes Nvidia AI Chip Smuggling Claims to China Seriously’. 7 February.

National Economic Advisory Council–Malaysia (NEAC). 2010. New Economic Model for Malaysia, Part I. Putrajaya: NEAC.

Ministry of Investment, Trade and Industry, Malaysia (MITI). 2023. New Industrial Master Plan 2030. Kuala Lumpur: MITI.

McKendrick, D. G., Doner, R. F. and Haggard, S. 2000, From Silicon Valley to Singapore: Location and Competitive Advantage in the Hard Disk Drive Industry. Stanford, CA: Stanford University Press.

Mukherjee, H. and Wong, P. K. 2011. ‘The National University of Singapore and the University of Malaya: Common Roots and Different Paths’, in Altbach, P. G., and Salmi, J. (eds), The Road to Academic Excellence: The Making of World-Class Research Universities. Washington, D.C.: World Bank, pp. 129–166.

Raj-Reichert, G. 2020. ‘Global Value Chains, Contract Manufacturers, and the Middle-Income Trap: The Electronics Industry in Malaysia’.Journal of Development Studies, 56/4, pp. 698–716.

Rasiah, R. 2017. ‘The Industrial Policy Experience of the Electronics Industry in Malaysia’, in Page, J. and Tarp, F. (eds), The Practice of Industrial Policy: Government–Business Coordination in Africa and East Asia. Oxford: Oxford University Press, pp. 123–144.

Rattanakhamfu, S. 2023. ‘Comment on “The Evolution of University–Industry Linkages in Thailand”’. Asian Economic Policy Review, Vol. 18, pp. 283–284.

Selvaratnam, V. 2016. ‘Malaysia’s Higher Education and Quest for Developed Nation Status by 2020’, in Singh, D. and Cook, M. (eds), Southeast Asian Affairs 2016, Singapore: ISEAS.

Sturgeon, T. and Kawakami, M. 2010. Global Value Chains in the Electronics Industry. Policy Research Working Paper 5417. Washington D.C.: World Bank.

______ 2011. ‘Global Value Chains in the Electronics Industry: Characteristics, Crisis, and Upgrading Opportunities for Firms from Developing Countries’. International Journal of Technological Learning Innovation and Development, 4/1, pp. 120–147.

Sultan Nazrin Shah. 2019. Striving for Inclusive Development: From Pangkor to a Modern Malaysian State. Kuala Lumpur: Oxford University Press.

Tham, S. Y. and Chong, P. Y. 2023. ‘Transforming Malaysia’s Higher Education: Policies and Progress’. Asian Economic Policy Review, Vol. 18, pp. 243–260.

Watkins, M. H. 1963. ‘A Staple Theory of Economic Growth.’ Canadian Journal of Economics and Political Science, 29, pp. 141–158.

World Bank. 2019. PISA 2018: Programme for International Student Assessment, East Asia and Pacific Regional Brief. Washington, D.C.: World Bank.

______ 2020. Who Is Keeping Score?: Estimating the Number of Foreign Workers in Malaysia. Kuala Lumpur: World Bank Group.

______ 2025. World Development Indicators 2025. Washington, D.C.: World Bank.